Storage Industry Research

West Ox Advisors diagnoses the magnetic data storage industry's chronic underinvestment in breakthrough technology, even at record profitability, and why concentrated markets produce exactly this result.

Publications

Breaking the Stalemate diagnoses the dynamic: a bilateral oligopoly in which suppliers rationally decline to fund breakthrough R&D, even at record profitability. Building on the vertical market failure (VMF) framework, the companion papers dive deep into two examples — one magnetic, one non-magnetic — to illustrate how the current market structure makes breakthrough investment nearly impossible, exactly the outcome VMF predicts. The Economics of DNA Data Storage examines the non-magnetic alternative that received the most funding to date, where DNA synthesis costs must fall orders of magnitude for the technology to compete — scientific work no existing capital structure is funding. Don't Mention HDMR examines the future of magnetic recording itself, where no Plan B to HAMR is funded as a committed development program. A single dynamic, visible on both sides of the technology frontier.

Flagship Paper

A formal economic argument that the magnetic data storage industry exhibits vertical market failure. A small group of hyperscale buyers facing a small group of suppliers systematically underinvests in breakthrough technology, even at record margins. The 2024 to 2026 period, with all-time-high profitability and roughly $11B in combined capital returns against zero non-magnetic R&D, serves as a natural experiment that confirms the diagnosis.

Companion Paper

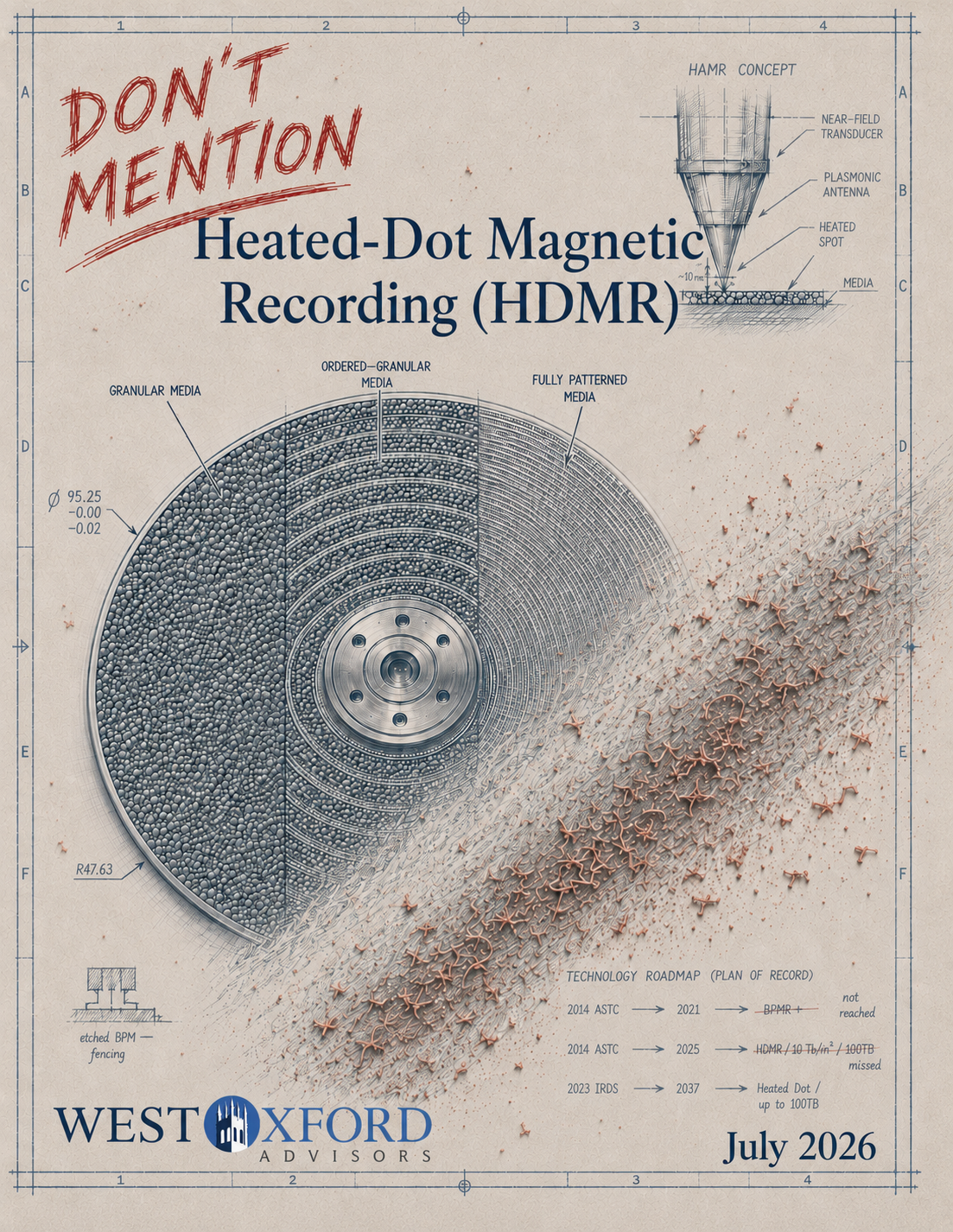

A November 2014 industry roadmap, signed by every major hard drive supplier, placed 100TB drives in 2025; the 2023 IEEE roadmap places them in 2037. This companion paper applies the vertical market failure framework to the technology that slip left behind: bit-patterned media, the successor to heat-assisted magnetic recording (HAMR) that no supplier today funds as a committed development program. The claim is not that bit-patterned media is required by a particular year, but that the absence of any funded alternative beyond HAMR is the vertical market failure thesis made concrete.

Companion Paper

The first application of the vertical market failure framework to a specific technology. Seven years after the Klusas 2019 MIST report, DNA data storage remains years from commercial viability, not because the science stalled, but because the capital structure that would fund synthesis cost reduction, among other elements, does not yet exist. The paper argues the burden has shifted to public and institutional capital, and that the field now holds the evidence and the coordination capacity to make a credible capital case.

The Challenge

Western Digital was the top-performing stock in the S&P 500 in 2025 with a 282% rally, and Seagate Technology was not far behind, posting a 219% gain. The records kept climbing into 2026: Seagate reported a record 47% gross margin, Western Digital crossed 50% gross margin for the first time, and both companies are effectively sold out of hard drives through 2026, with long-term agreements reaching into 2027 and 2028. Prices rose another 10% in the second quarter of 2026 alone, analysts now warn the shortage could extend to 2028, and demand forecasts project 25%+ annual storage growth through 2030. Yet the manufacturers' answer to the shortage is not new factories: capital spending sits at the bottom of both companies' target ranges, and when an analyst asked whether customers might co-invest in capacity, Seagate management pointed instead to capacity gained through product transitions — more terabytes per drive, not more drives.

By mid-2026, Seagate and Western Digital, the two publicly traded manufacturers of hard disk drives (HDD), carried a combined market value of more than $400B, up from roughly $118B six months earlier, while research and development spending crept up only single digits against surging revenue, falling to multi-year lows as a percentage of revenue. Toshiba, the third HDD supplier, is privately held and is not reflected in that figure.

In the context of this record financial performance, magnetic storage manufacturers chose financial engineering over breakthrough innovation. Seagate announced a $5B share buyback program and Western Digital authorized $6B in buybacks across two programs, a combined $11B committed to shareholders. HAMR extensions are Plan A. There is no funded Plan B: no successor technology, magnetic or otherwise, holds a committed development program with committed dates, even as a hedge.

The cost of that choice is written in the industry's own roadmaps. A November 2014 roadmap, signed by every major hard drive supplier, placed 100TB drives in 2025. The 2023 IEEE roadmap places them in 2037. This is vertical market failure in action, and it is why the AI boom changes nothing: the on-going 2024–2026 period is the most favorable demand environment the industry may ever see, and it still has not produced a single funded breakthrough program. If record margins, sold-out capacity, and guaranteed demand cannot unlock long-term, novel R&D bets, then demand was never the missing ingredient.

The AI boom is not the cause of the vertical market failure, and it will not be its cure. Whenever the party ends, the vertical market failure will still be sitting there, because the bilateral oligopoly structure of both hard drives and magnetic tape prevents the capital pooling that breakthrough development requires.

What You'll Learn

Breaking the Stalemate

How economic theory explains the storage industry's innovation paralysis, and why traditional competitive dynamics can't solve it.

Breaking the Stalemate

Record profitability and favorable market conditions provided a definitive test: suppliers chose $11B in share buybacks and dividends over breakthrough innovation, with R&D falling to multi-year lows as a percentage of revenue — validating the VMF thesis.

Breaking the Stalemate

A detailed case study of how the semiconductor equipment industry faced and solved an analogous market failure through strategic customer collaboration.

Breaking the Stalemate

Concrete paths forward for storage companies, hyperscalers, and investors seeking to break the stalemate and capture the next wave of value.

The Economics of DNA Data Storage

Synthesis costs must fall by orders of magnitude for DNA storage to compete, and no capital structure exists to fund that work, shifting the burden toward public and institutional capital.

Don't Mention HDMR

100TB drives were promised for 2025; the current IEEE roadmap says 2037. No successor beyond HAMR is funded as a committed development program, not even as a hedge.

In the Headlines

Speaking Engagements

For decades, computing drew on a shelf of demonstrated, but undeployed technology, stocked largely by government-funded research. That shelf is being consumed faster than it is replenished. This panel examines magnetic data storage – hard drives and magnetic tape – a bilateral oligopoly with a few suppliers facing a few dominant hyperscale buyers. The result is a vertical market failure: suppliers rationally decline to fund breakthrough R&D they cannot be certain of recouping. The 2024–2026 period illustrates the point: record margins and $11B in authorized buybacks, while prices rose 46%, lead times stretched past a year, and no next-generation technology received funding. The market still lacks a tier combining tape's low cost with quick access. The panel debates whether the same stall threatens other computing technologies and closes on two questions: what will HPC, AI, and long-term archives require, and who will fund the technology to deliver it?

Panelists

Gary Grider, Los Alamos National Laboratory

Candace Culhane, Los Alamos National Laboratory

Steffen Hellmold, Cerabyte

Matt Klusas, West Ox Advisors (moderator)

Matt Klusas presented on the vertical market failure thesis and potential co-investment models at MSST 2026, the International Conference on Massive Storage Systems and Technology.

View MSST 2026 →

Peter Faulhaber presented West Ox Advisors' vertical market failure research at Venture SPRIN-D 2026, the annual showcase organized by Germany's Federal Agency for Disruptive Innovation, connecting investment-ready deep-tech teams with leading global investors. The session fell within COMPUTA, the compute infrastructure track.

View Venture SPRIN-D 2026 →Matt Klusas presented the white paper's findings at the Motor Drive Systems & Magnetics Conference, alongside speakers from NASA, Tesla, the Department of Energy, and leading research institutions.

View MDSM 2026 Program →